The AI timeline is loud right now. Revolution. A new industrial age. A jobs apocalypse, or nothing to worry about at all, depending on whose post you read. Before picking a side in that, one question is worth asking: how often, in human history, has a single technology reorganized the entire economy? Not improved a sector. Reorganized the whole thing.

I keep coming back to this with my students. Almost everything that gets said about AI depends on the answer, and almost no one arguing about it online stops to ask it.

Economic historians have spent decades on it, and they more or less agree. In five hundred years, it happened four times. Just four times.

The first one was the printing press, somewhere around the 1450s. The second one, the steam engine, in the late 1700s. Electricity came third, at the end of the 1800s. And finally, computing and the Internet, starting in the second half of the twentieth century. That is the entire list.

And we are living through the fifth.

What it means for a technology to be that rare

The category has a name. Economists call them General Purpose Technologies (GPTs from now on), and the modern definition comes from a 1995 paper by Timothy Bresnahan and Manuel Trajtenberg called, fittingly, “Engines of Growth?”. I’m going to borrow their word. When I say engine in this piece I mean exactly that, an engine of growth: a GPT that powers a whole economy and pulls a shelf of later inventions along behind it. That is, the economy’s engine, not a loose metaphor.

A GPT is more than just a useful invention. It has three properties at once, and it needs all three to qualify.

The first is that it is pervasive. It does not improve one sector, it shows up in almost all of them. The steam engine was not a mining tool that escaped the mine. It moved into textile mills, ships, railways, printing presses, agriculture, and the back room of every factory that did anything mechanical. Electricity spread the same way a hundred years later, and computing did it again.

The second is that it keeps improving for decades. A real GPT does not stop getting better the year after it is introduced. Steam engines were thirty times more efficient in 1900 than they were in 1800. Electric motors got smaller and cheaper for a century. Microchips have been on Moore’s curve since 1965. The runway is long, and that long runway is what lets the technology spread.

The third property, and the most important, is that a GPT spawns other inventions. It enables technologies that could not exist without it. The steam engine made the railway possible, which made national markets possible, which made retail brands possible. Electricity made the elevator possible, which made tall buildings possible, which made modern cities possible. Take any one of these engines away and a whole shelf of later inventions never happens.

That is a much higher bar than “important new technology”. Most things never clear it. The car is huge, but it is not a GPT in the technical sense. Neither is the airplane. The smartphone is arguable, depending on who you ask. The bar is high, and that is why the list has stayed short for five hundred years.

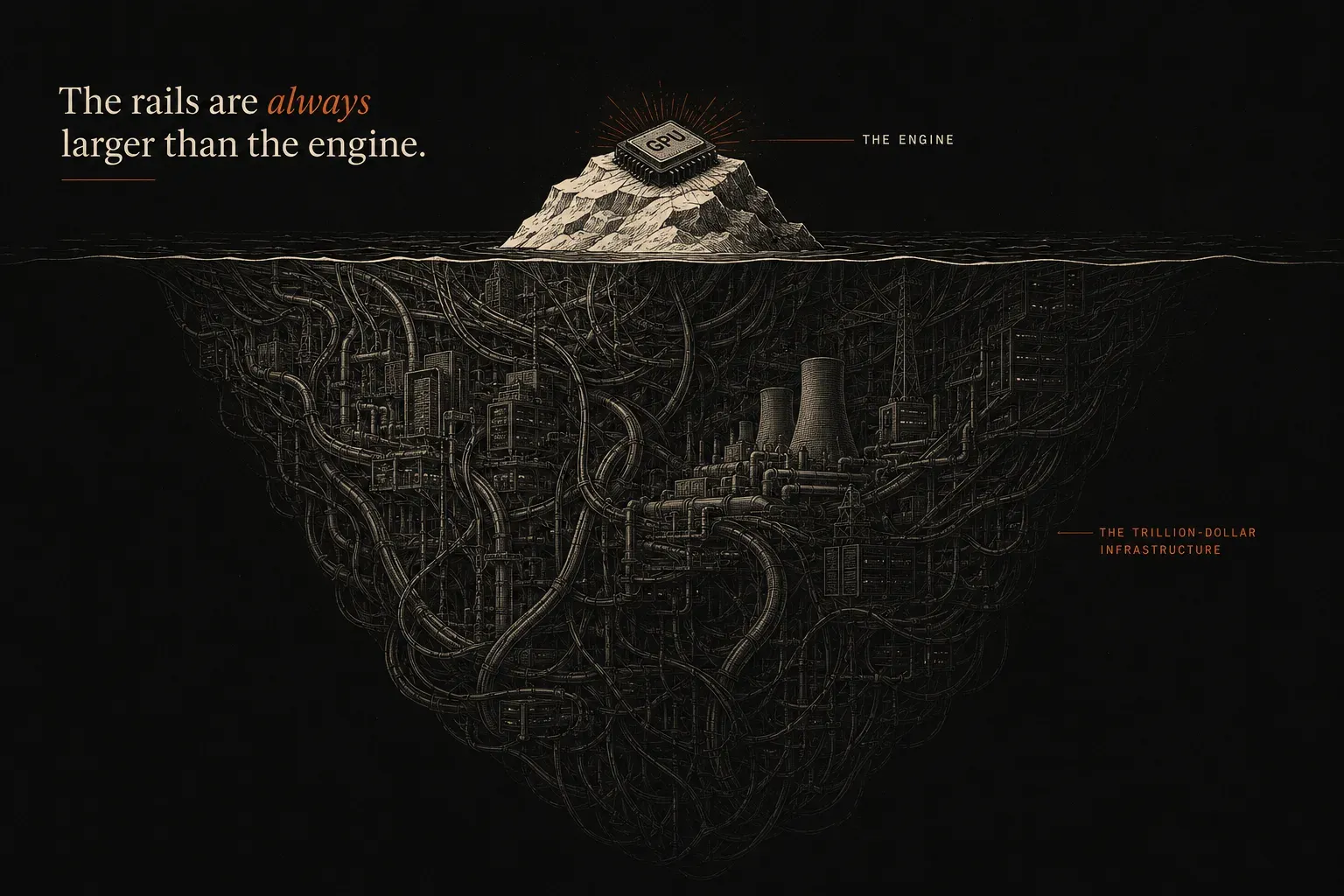

Every engine arrived with a body to run on

The four share something else. Each arrived with a piece of infrastructure roughly the size of the technology itself.

The printing press needed paper at scale, printing workshops, and distribution networks for books. None of those existed in 1440. The steam engine needed railways, canals, coaling ports. The first British rail boom in the 1830s was, in effect, the country building a body for the engine. Electricity needed the electric grid, a project so big it took the better part of fifty years to roll out across a single country, plus power plants, plus rewiring every factory and home that wanted to use it. Computing needed cables. First copper, then fiber, then mobile networks. The Internet looks like it lives in the air, but the actual cables that carry it span every ocean on the planet.

That infrastructure is the part that does not feel sexy at the time. Most contemporaries underestimate it. They argue about the engine itself and ignore the rails it has to run on. The infrastructure is also where the real money goes.

AI is following the same pattern. The infrastructure of this fifth engine is datacenters, GPUs, and the electricity to power them. We are deep enough into the buildout that the numbers stopped sounding like software economics. OpenAI has reportedly laid out a five-year plan to meet a trillion dollars in spending commitments. Hyperscalers have already outspent the most famous American megaprojects of the twentieth century. Microsoft has signed a twenty-year power purchase agreement with the restarted Three Mile Island nuclear plant. Google, Amazon, and others have inked their own nuclear deals. Eric Schmidt, the former Google CEO, recently named the real bottleneck. It is not energy, he said. It is cash. Roughly fifty billion dollars per gigawatt, by his estimate. Ten gigawatts gets you to half a trillion.

If this engine looks expensive, that is because all the previous engines were expensive in their own time. The numbers are just larger, and the timeline is shorter. But the comparison has a twist worth sitting with. The hyperscalers have outspent those megaprojects in raw dollars. Measured against the size of the economy, though, the old engines were bigger. The railroad build-out of the nineteenth century peaked at several times AI’s current share of GDP, roughly four to six percent against AI’s one and a half. The most expensive buildout in absolute history is still, as a fraction of the economy, smaller than the railroads once were. If AI is a real engine, that is not a sign the spending has gone too far. It is a sign that it is early.

What each engine did to work

The four GPTs we have lived through did not all do the same thing to work. They affected the economy in different ways, and the difference is worth understanding before talking about the fifth.

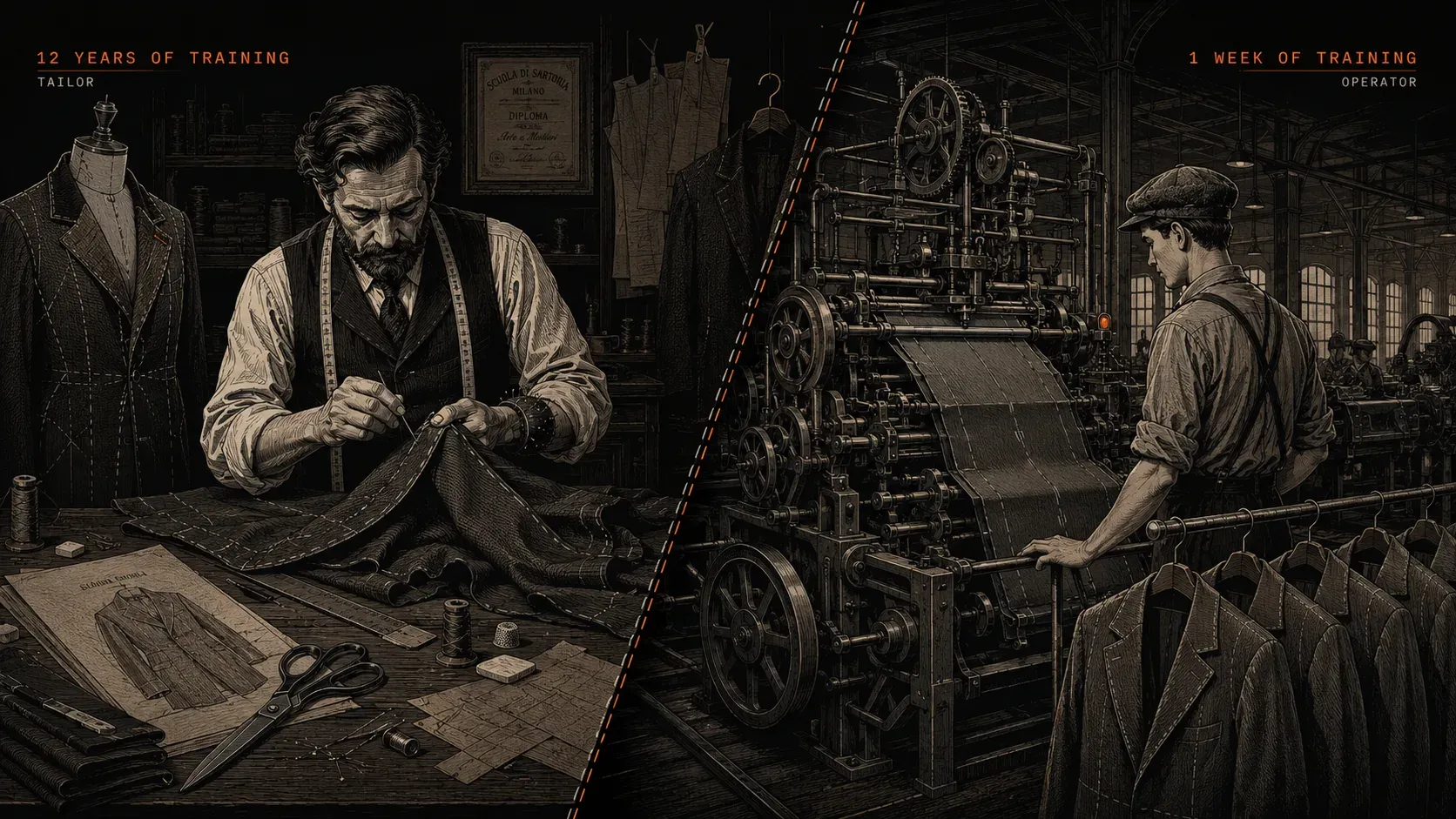

Steam and electricity, the first two big industrial GPTs, did something specific. They raised global GDP, that part is well known. But they also lowered the barrier to entry into work.

Think about the tailor of 1750. To make a coat for a customer, the tailor needed years of guild-controlled apprenticeship, deep knowledge of cloth, cutting, fit, hand-finishing. The skill was scarce, and the scarcity was the whole point. Then the steam-powered textile mill arrived. It did not need the tailor. It needed a machine operator, who could be trained in days. The skill that took twelve years to master became a skill that took only a week. Millions of people who were previously locked out of the workshop walked into the factory. Global output went up, and the gains spread across a much wider workforce. Electricity, fifty years later, did the same thing. Taylorized factories, assembly lines, division of labor pushed even further. Same dynamic, bigger scale.

That is the pattern people have in mind when they say industrialization “created the middle class”. GDP grew, the floor of who could work grew with it, and the gains were broadly distributed, at least eventually, at least roughly.

Then computing and the Internet arrived, and the pattern broke.

Computing produced the largest GDP jump of any of the four. The United States economy is fundamentally different in 2026 than it was in 1970, and most of that delta comes from information technology. But this engine did not lower the barrier to participating in the new work. On the contrary, it raised it. To operate a mainframe, you needed not a week of training but a four-year computer science degree. The same was true for the Internet, for software, for data science. The skills are deep, expensive, and hard to acquire. The gains of the new GPT concentrated in the people who had those skills, and in the companies that could hire them at scale.

This is not abstract economics. It shows up in the data, and it shows up in a chart that Erik Brynjolfsson and Andrew McAfee made famous in their book The Second Machine Age. They called it the Great Decoupling.

The Great Decoupling

The chart plots four lines over the second half of the twentieth century. Labor productivity. GDP. Private employment. Median family income. From 1947 until about 1980, the four lines move together. The economy grows, productivity grows, employment grows, and household income grows along with them. They are essentially the same curve.

Around 1980, two of the lines keep going up. The other two begin to flatten out.

Productivity and GDP continue to climb, almost as if nothing had changed. Employment growth and median household income begin to lag, and the gap widens for the next half century. That is the decoupling. The economy keeps producing more, and most of the people inside it stop seeing it in their paycheck.

The economists argue about how to measure it. The size of the gap depends on the deflator you use, on whether you count benefits, on what you consider median. Fair enough. But the qualitative point is robust across the methods. Output and median compensation, which used to move together, stopped moving together a few generations ago.

The timing is not a coincidence. It maps roughly onto the consolidation of computing as a general-purpose technology, and onto the moment when the most valuable work in the economy started to require the kind of training that not everyone has access to. A GPT with a high entry barrier concentrates the gains it creates. That is what the chart is showing.

If you have spent the last decade arguing about wages, inequality, the hollowing out of the middle class, or any of the related questions, you have been arguing about, in part, the second-order effects of the third GPT.

So which kind is AI?

Here the easy answers stop working.

If AI follows the steam-and-electricity pattern, it lowers the barrier to participating in skilled work. A junior with an AI assistant produces what a senior used to produce alone. People who cannot code ship software, people who cannot design ship visual work, people who never learned a second language work across them anyway. The skill stays valuable, but acquiring it stops requiring a decade. If that is the path, the economic outcome of AI will look more like 1850 than 1990. Output, as in every GPT, will go up, and the gains will spread across a wider workforce.

If AI follows the computing pattern, it raises the barrier. The really valuable work moves to the people who can orchestrate complex AI systems, design model architectures, and build the infrastructure underneath. Everyone else is supervising, or doing the residual tasks that the systems do not yet handle. If that is the path, the Great Decoupling will continue, and will probably accelerate.

We do not know yet. Unfortunately, the evidence is mixed and recent.

On the “lower barriers” side, there is real data. A study of consultants at Boston Consulting Group given access to GPT-4 found that the AI-assisted group did about 40 percent better quality work, and that the gap between top and bottom performers within the group narrowed by 43 percent. The biggest gains went to the people who started out below the median. That looks like steam and electricity. It looks like a leveling technology.

On the “concentrate the gains” side, there is also data. Anthropic’s own labor market study found that AI exposure is strongly concentrated in white-collar work, with junior roles being affected first. A recent paper out of the LSE finds that early-career hiring in AI-exposed occupations is already declining. Klarna spent 2024 celebrating that its AI assistant replaced the work of seven hundred customer service agents, and 2025 quietly admitting it had cut too deep and was hiring humans back. The picture is not clean.

And then there are the people whose job it is to bet on the answer. Dario Amodei, the CEO of Anthropic, has said publicly that he expects AI to eliminate roughly half of entry-level white-collar work in the next one to five years. Andrew Ng has said, almost as publicly, that the “AI jobpocalypse” story is irresponsible and that the data does not support it. Sam Altman has asked, in writing, for the data behind Amodei’s number. Two billionaires running two of the most important AI labs in the world cannot agree on whether the technology they are building will keep the middle of the labor market or break it. That is where we are. And in the last few weeks it got stranger: both of them softened their own warnings inside the same three-week window in May 2026. Amodei, who had warned of a white-collar bloodbath, reframed it as more work, not less, and Altman said he was “delighted to be wrong” about the jobs apocalypse he once predicted. Each pivot landed almost exactly when his lab filed confidentially to go public, while tech layoffs that same month kept climbing. They cannot even agree with themselves.

What I tell my students is that you do not have to pick a side today. You have to understand that this is the real question. Not “is AI useful?” (yes, it is, and quite a lot, obviously). Nor “will it change work?” (yes, it already has). It is whether the fifth engine looks like the second one or like the fourth one. Those two paths end up in different places, and most of the noise online is about the wrong one.

Why this matters now

One thing makes this engine different from the previous four, and it is not capability. It is speed.

The previous GPTs took a long time to play out. Steam took roughly fifty years to fully transform the economies it touched. Electricity took something similar, maybe a bit faster. Computing has been working on us for sixty years and is arguably still in the middle of its run. Half a century is the rough number.

AI is not going to take half a century. For a model of equivalent performance, the cost of running it is falling by roughly an order of magnitude per year, and that is the conservative end of the published estimates. Models that were research papers in 2022 are products in 2024 and infrastructure in 2026. The infrastructure buildout that the previous GPTs spread across decades is being compressed into single-digit years of capex. Adoption is happening faster than any of the previous engines, by a wide margin. Elon Musk’s phrase for it is “AI is a supersonic tsunami”. It is a good description of the speed.

The transition might be half a decade, not half a century. That is the part that should make managers and policymakers nervous. Not because of the destination. The destination, on a long enough horizon, is probably fine. The previous GPTs all created more work than they destroyed, eventually, even when they were brutal to the people stuck on the wrong side of the transition. The reason to be nervous is that we may not have time to be slow about this.

If you are running a team, leading a function, building a company, advising one, or just trying to plan a career, you do not need to predict which path the fifth engine takes. You need to be ready for either one. Get good at orchestrating these systems now, instead of waiting to see which way it breaks. And stop treating AI as just another tool.

The first four engines all looked, at the time, like just another tool. They were not.

This is the fifth.

Sources

- Timothy F. Bresnahan and Manuel Trajtenberg. General Purpose Technologies “Engines of Growth?” Journal of Econometrics, 1995. The canonical definition. Read the paper.

- Jeremiah E. Dittmar. Information Technology and Economic Change: The Impact of the Printing Press. Quarterly Journal of Economics, 2011. The printing press as a pre-industrial GPT. Read the paper.

- Richard G. Lipsey, Kenneth I. Carlaw, Clifford T. Bekar. Economic Transformations: General Purpose Technologies and Long-term Economic Growth. Oxford University Press, 2005. The full catalogue of historical GPTs. Review.

- Erik Brynjolfsson and Andrew McAfee. The Second Machine Age. W. W. Norton, 2014. Where the “Great Decoupling” chart was introduced and named. A version of the chart and a short summary is here. For the empirical debate about magnitude, see the Resolution Foundation review.

- Kai-Fu Lee. AI Superpowers: China, Silicon Valley, and the New World Order. Houghton Mifflin Harcourt, 2018. On the democratization of AI capability and what it implies for the global labor market. Goodreads page.

- Anthropic Economic Index. Labor market impacts of AI: a new measure and early evidence. March 2026. The empirical study underneath the “asymmetric finding” point.

- On the absolute scale of the buildout: Fin Moorhouse, “The hyperscalers have already outspent the most famous US megaprojects,” chart compiled from Epoch AI data. Post on X.

- On the buildout as a share of GDP, where the historical engines were larger: Tomasz Tunguz, “Are We Being Railroaded by AI?” (Theory Ventures), and Kai Williams, “16 charts that explain the AI boom” (Understanding AI). Railroads peaked near four to six percent of US GDP; AI infrastructure is running about one and a half percent. Tunguz, Understanding AI.

- Guido Appenzeller, “Welcome to LLMflation: LLM inference cost is going down fast,” Andreessen Horowitz (a16z), November 2024. “For an LLM of equivalent performance, the cost is decreasing by 10x every year.” Read it.

- “Sam Altman and Dario Amodei are both walking back their AI jobs apocalypse prophecies as they eye blockbuster IPOs,” Fortune, May 2026. Both reversals, with the IPO-timing framing. Read it.

- Elon Musk, “AI is a supersonic tsunami,” on X, 21 January 2026. Post. He used the same phrase on Joe Rogan’s podcast in November 2025.